Where Will Opportunistic Investors Find Great Buys in Real Estate?

Part 1: Short Term Rentals

When the Covid crisis first hit, and the economy first shut down, my brain immediately went from apprehensive on the future of my own businesses, to thinking about how the shut down will trickle up through the economy, to thinking about which real estate sectors will be hurt the most. And then…to where there may be opportunities. Big opportunities.

I’m clearly not the only one who thought this way, as the stock market immediately rebounded from the lows; buyers swooped in to acquire shares at deeply discounted prices. I believe these actions were fueled by the lessons learned from the 2008 Great Recession. Many people had the mindset of wanting to identify great buying opportunities, and take action, this time, unlike the last.

This article isn’t about stocks, but I do believe the pendulum swung way too far, and that the bottom will fall out of the stock market again. The economy is deeply troubled, and will continue to be, and the current valuations make no sense.

What I do want to outline is the process that I believe will unfold over the next 12-24 months in the commercial real estate market.

When the economy shut down due to Covid, my hypothesis became: Owners of short-term rentals would be the first to get hurt, and will lead to short sales and foreclosures of what may be very attractive assets. My logic:

Many first-time investors have leveraged up, buying multiple properties at prices that only make sense if they can keep them highly occupied as short-term rentals. They are running hotels, except without the economies of scale that an actual hotel provides.

If they had to convert to long-term rentals, they would not be able to cover their debt obligations.

Many of the short-term rentals in San Diego are in neighborhoods that make very little sense to me. It is one thing to rent a house in La Jolla for a vacation, but I was seeing them in lower income neighborhoods, without walkability or nearby amenities. And many of these short-term rentals were performing very well.

The primary driver of short-term rentals is the discount from traditional hotels, plus having a kitchen and often multiple bedrooms.

But with hotels at low occupancy, rates have dropped, making the arbitrage less attractive for vacationers – so I believe they will return to hotels, not homes

A concern about cleanliness – would you put more trust in a hotel staff’s cleaning crew to disinfect a room after each stay, or a homeowner / AirBnB host?

These owners are highly leveraged, and are more likely to let the properties go into foreclosure; the banks are less likely to work out forbearance agreements for 2nd home / investment properties. The banks will have much bigger problems looming in other real estate asset classes.

To be clear, many or even most short-term rentals should do fine once the economy opens up. But if overall travel, after the “new normal” is established, is down say 10%, or 20%, that will hurt the worst properties. But targeting the worst vacation rental could still be a great buying opportunity.

The Opportunity This will not be a 2008 scenario. Opportunistic investors will need to seek out the opportunities, create their own opportunities.

How these will hit the market: Through Short Sales and Foreclosures. Owners / Operators of multiple short-term rentals, unable to meet their mortgage obligations, will eventually need to put them up for sale. If they bought at the peak, they may sell for a discount to the mortgage principal.

When: In the next 6-12 months. Currently, lenders are offering forbearance on debt obligations, and owners are still hanging on. Give this a little bit of time. But…I’m predicting this asset class will be the first down leg in the commercial property downturn.

The reason short-term rentals will fail first, is that lenders will have bigger problems looming. Large retail centers, malls, hotels, and office buildings will be a bigger priority for loan modifications and work outs. The traditional short sale / foreclosure process will hit the short-term rental asset class first.

How Investors Can Take Advantage: Do not wait for the properties to be listed for sale. That is what everyone does. Here’s the playbook:

Create a list of your favorite properties. Go on the short-term websites and grab as much data as you can. Addresses are often obscured, but not on all sites. You’ll have to be resourceful. No one said this is easy, are you going to be the one who does the work?

Pull public data on the mortgage principal, and compare it to the value of the property. The highest-leveraged properties will be the most likely to go to short sale or foreclosure.

Reach out directly to the owners. You want to be the one they call when they decide to sell, or are forced to sell

Uncomfortable doing all of the above? This is what brokers do. But once a broker has a listing, their goal is to sell for the highest price possible – the opposite of your goal. Consider forming an alliance with a broker, who will do the leg work to find you the opportunities

Be disciplined in your underwriting and execution.

Who should pursue this asset class: Smaller investors, looking to pick up a 1 to 3 properties. This will be a difficult model to scale. If you own apartment buildings, buying a single unit or two may not be very attractive. Those investors will be pursuing the asset classes and strategies I will outline in future articles. But if you’re starting to build a portfolio, this is a great place to start.

Word to the wise: These opportunities will arise because the assets did not pencil as long-term rentals, the buyers assumed the world would not change and short-term rentals will be a going concern. Now the supply / demand for vacation stays is different. And cities have been introducing regulations limiting short-term rentals. So be sure your acquisition pencils as a long-term rental. If you can convert it back to short-term in the future, that will be extra profit for you. This is a sub-series within my “Investment Strategies for a Post-Peak Economy” series of blogs.

I will examine each of the following asset classes in real estate: short-term rentals, hotels, retail centers, office buildings, multi-family, and the residential for-sale market. I will skip industrial and land asset classes, as I believe those are very site-specific and not subject to the same overall market dynamics.

I welcome feedback, and please share intelligent articles you come across on these subjects. I’m still studying this and welcome intelligent dialog.

About MV Properties and Keegan McNamara: MV Properties exists to serve our clients in building their wealth through real estate investments. We guide our clients through creating customized real estate investment strategies. We analyze our clients’ portfolios, looking at return on equity (ROE), debt strategies, and tax efficient planning, to develop a plan specific to each clients’ needs. We let the numbers tell us the strategy, as each situation is different.

Keegan McNamara is a real estate investor, developer, and broker. He owns MV Properties, a residential brokerage and property management firm, and McNamara Ventures, a development and investment company. Keegan can be reached at keegan@mcnamaraventures.com

Part 4 in a Series: Investment Strategies for a Post-Peak Economy

The least understood real estate asset class is Land. This blog post will take a deep dive into how real estate developers and home builders value land. And it will describe the risks and rewards in this very specialized asset class. Land investments are not for the faint of heart!

The Wrong Way to Value Land:

Simply pulling “land comps,” which many inexperienced realtors use when marketing an undeveloped property, is fundamentally flawed.

Looking at comparables – “comps” – works for two homes that are similar size, in the same neighborhood. But land has many other variables.

This is because the cost to grade, to bring utilities to the site, for any mitigation needed, and for the level of on-and-off site improvements – these all vary greatly from one development to the next. One property may need large retaining walls, another may require undergrounding of utility lines.

Not to mention zoning. A small parcel in an urban area that is zoned for mid-or-high rise construction will have more value than a small parcel zoned for a single home.

So the comps method of valuation typically does not work to value land. The exception is when two very similar properties, with the same underlying zoning, have recently sold.

How Home Builders Value Land:

Because of the different characteristics of undeveloped land, home builders value land using a Land Residual financial model.

Early in my career, a mentor described it to me simply: Land value is based on what income one can derive from the land. It’s that simple – yet to get that answer can be complex.

For residential land, we work backwards and start with the estimated value of a hypothetical finished home. “If I built a 3,000 s.f. home on a ¼ acre lot, what would it sell for?” This should be relatively easy to solve, based on the home sale comps in the area.

If a 20-year old neighboring home recently sold for, say $800,000, then I can reasonably expect a new home of similar size will sell for $900,000 or more. Buyers will pay a premium for a new home. But in my underwriting for a land acquisition, I’ll usually use $800,000 as my finished home value, in order to be conservative and protect against downturns.

The builder then subtracts all of the costs to build that home, and subtracts their financing costs, and their projected profit margin, and the residual of that simple equation is what they can afford to pay for the land:

Finished home value minus all costs to build minus financing costs minus profit = residual land value of an undeveloped lot.

Turn this equation around in order to look at it from the home builder’s perspective:

“If I can sell an $800,000 home that I know costs $494,000 to build, finance, and pay all the consultants, and after I pay $50,000 in government fees, my profit will be $96,000 per home – 12%.”

Using this equation and the above assumptions, a fully “entitled” lot is worth $160,000:

Entitlements are loosely defined as the legal right to build on the land. In California, this is typically a long approval process through the City or County that has jurisdiction of the property.

When a property is subdivided, meaning one legal parcel is legally divided into five or more parcels, that is referred to a Tract Map (TM). A TM will come with Conditions of Approval that must be met prior to the owner/developer recording a Final Map. These conditions typically include right-of-way dedications, street improvements like stop lights and street widening, sidewalks, and landscaping.

The tentative map is a legally binding document and allows the builder to move forward towards final engineering and pulling building permits to start construction. Therefore, an approved Tentative Map is typically what is referred to as an entitled property.

For smaller projects, where the builder’s proposal meets all the zoning guidelines, an “entitlement” can even be as simple as administrative approval of the conceptual design, needing only City or County staff approval, and avoiding the longer process of Planning Commission or City Council approval.

For Land Developers, we aim to add significant value to a property by going through this process.

Going back to the example above, if a home builder were to pay $160,000 for an unentitled lot, they would lose money in building the home. That is because they did not adequately factor in the cost, time, and risk of getting through a local City’s approval process.

For a typical residential subdivision, the land developer will need to hire the following consultants: civil engineer, multiple environmental consultants, utility consultants, historical consultants, cultural resource consultants, plus traffic, fire, and many others. And, the jurisdiction that grants a Tract Map approval will have their own application and processing fees.

Add these up, and the typical subdivision approval costs a multiple of six figures in California. And that’s if things go relatively smoothly, and the land developer is following the existing zoning.

When one proposes a zone change, or a development near the coast, or anything with sensitive habitat or environmental concerns, then hold on to your hat. The cost can then climb into the seven figures, and take many, many years.

The risk side also needs to be considered: if the land developer’s proposed use is not approved, but he/she paid top dollar assuming the entitlements would be quick and easy, they will quickly be underwater.

Often home builders avoid the entitlement process, because it’s not what they do best. It’s highly specialized, takes a lot of time, and involves a lot of risk. Homebuilding is risky, too, of course. But that is their specialty and they will typically look to acquire land after the legal entitlements are approved.

Paper Lots to Blue Top Lots to Finished Lots

After land entitlements are approved, the land developer then has options: build the proposed project themselves, sell the land and all the legal entitlements to a home builder, or enter into a joint venture with a builder.

When selling the land outright, it is typical for smaller land developers to sell “as-is” and not put any improvements into the land.

In large master-planned communities, however, the land developer will often grade the lots, to what is referred to a “blue top” condition. A home builder may buy based on that level of finish, or if the master developer puts in the roads, curbs, and gutters, and stubs utilities to each fully graded site, then that is a “finished lot.”

This is important, because the “finished lot” is a crucial value in negotiations for the land developer to sell to the home builder.

The reason for this, is that once a lot is “finished,” the builder can quickly determine the costs to pour the foundation and build the home. Builders typically repeat floor plans and have strong data from their previous subdivisions. Vertical construction is much more standardized, whereas the costs to get to a finished lot will vary greatly from subdivision to subdivision.

Completing the Land Residual Model

A good rule of thumb is that a “finished lot” is typically worth 35% – 45% of the anticipated finished value of the completed home.

So from this “finished lot basis,” the cost of all grading and site work, and government fees, are subtracted, to calculate a “paper lot value.”

This is what the Land Developer will often sell – paper lots.

Example of a Land Residual Value

Based on the methodology above, and the assumptions below, a land developer will anticipate selling “paper lots” for approx. $160,000 per lot.

Note that every dollar difference in the Lot Finishing Cost is a 1-to-1 difference in the paper lot value. So if the cost is actually $100,000 per lot instead of $110,000 per lot, then the paper lot value will go up from $160,000 to $170,000. The inverse is also true.

Should Real Estate Investors Invest in Land Development?

As noted at the beginning of the article, land development is a highly specialized asset class within real estate investing. I do not recommend investing in this asset class unless: 1) the Developer with whom you are investing has many years’ experience processing tract maps and going through the entitlement process, , and 3) the Investor is very comfortable taking a passive position in an illiquid asset.

Other reasons to not invest in land:

Typically, the land generates zero cash flow. So during the entitlement phase, there is no income to pay consultants, property taxes, or loan payments if the owner uses leverage. All the cash needed will come from equity investment, not the property, unlike say, an apartment.

During recessions, if builders stop building new homes, there may not be a buyer for the land after the entitlements are approved. This could mean sitting on the land for much longer than originally anticipated, and must be factored into the business plan. Or if the owner needs to sell, they risk selling at a deep discount, in a distressed sale scenario

Scenarios where land investment is appropriate:

The investor is partnering with an experienced land developer

The land basis – the price they pay for the dirt – is low enough to absorb economic downturns

The investor is highly liquid and/or invested in other asset classes that generate cash flow. If they may need the money in less than a few years’ time, the investor should stay away

From an asset allocation standpoint, land should be in the “speculative/risky” bucket. A successful project may double the investor’s money. But when these types of investments go wrong, they can have the opposite outcome

Conclusions:

The land entitlement process in California is highly regulated, time consuming, and expensive.

The value of land is determined by the income that the owner or developer can derive from it, typically calculated through a land residual model. Comps work very poorly in valuing land.

Investors should be very cautious when investing in this asset class.

McNamara Ventures is currently managing two residential subdivision investments in San Diego County.

Our partnership includes Oscar Uranga, a land entitlement guru with IMG Construction Management, and a sophisticated group of investors.

We are being highly selective in future land investments.

About McNamara Ventures, MV Properties, and Keegan McNamara:

McNamara Ventures and MV Properties exist to serve our clients in building their wealth through real estate investments. Services include: investment offerings, property management, and boutique brokerage.

We guide our clients through creating customized real estate investment strategies.

We analyze our clients’ portfolios, looking at return on equity, debt strategies, and tax efficient planning, and develop a plan specific to each clients’ needs.

We let the numbers tell us the strategy, as each situation is different.

Keegan McNamara is a real estate investor, developer, and broker. He owns McNamara Ventures, a development and investment company, and MV Properties, a residential brokerage and property management firm. Keegan can be reached atkeegan@mcnamaraventures.com.

Part 3 in a Series: Investment Strategies for a Post-Peak Economy

Andrew Carnegie famously said that over 90% of the world’s millionaires made their fortune by investing in real estate. I don’t know how true that statement is, but Forbes states that 10% of the world’s billionaires made their fortune by investing in real estate. 1

One of the primary ways to build wealth is through wise investing that compounds over time. Real estate is perhaps the best way to build wealth.

This article, Part 3 in a series, examines the 5 ways that real estate investors make money.

1. Cash Flow.

Simply put, strong commercial real estate investments should generate annual cash flow, after paying all the property’s operating expenses, taxes, insurance, and mortgage.

In this article, I go into much greater depth as to why this should be the most important metric for real estate investing today. If your real estate assets are not generating cash flow, you really should read the article.

2. Equity growth through leveraged appreciation

When a stock appreciates, the value of each share goes up. The same holds true for real estate, although the added benefit is leverage, which amplifies the investor’s return.

Take the following example:

A $400,000 property, purchased with a $100,000 down payment.

Over time, the property may increase in value, say 10%, to $440,000. That’s great, but even better:

The Investor’s return is actually 40%. The bank that loaned the $300,000 mortgage does not participate in the price appreciation of the property: the $40,000 appreciation / $100,000 down payment = 40% 2

NOTE – the risk of deprecation, when an asset’s value decreases, also magnifies the potential losses. These risks can be minimized through strong cash flow.

Understanding Cash-on-Cash The term “cash-on-cash” is an important metric in real estate that is worth noting here. Prior to selling the asset, our cash-on-cash is the annual cash flow before taxes, but after all operating expenses, divided by our original down payment amount. When we sell the asset, we then combine the total cash flow of the property with the 40% return (our total cash out), and divide that by the original down payment plus improvement costs (our total cash in) to get our total cash-on-cash return. In non-real estate finance world, this metric is usually referred to as Return on Equity, ROE.

3. Equity growth through tenants paying down the loan principal

Using the same example above, after the first five years of ownership, the principal balance on the original $300,000 loan is now just over $275,000!

Here is the loan amortization schedule for a $300,000 mortgage at 5% rate on a 30 year loan:

Having tenants pay rent in commercial buildings contributed an additional $25,000 in equity growth over the original $100,000 down payment.

So when combined with the 40% equity growth through appreciation, the $400,000 property that sells for $440,000 in year 5 has returned a total profit 3 of $64,514 on the original investment of $100,000.

That’s a 64.5% return over 5 years, just under 13% per year. And it is not an aggressive assumption whatsoever – it assumes asset prices appreciate at only 2% per year, right around the Fed’s target inflation rate for the U.S. economy.

This leads us to the 4th way real estate investors make money:

4. Inflation

Inflation helps real estate investors in three different ways.

Using the same example above, let’s say that real estate appreciates slightly higher than U.S. inflation, and the asset value goes up 3% per year. In Year 5, that’s a 15% total appreciation.

That $100,000 original investment has generated a 60% return, before we include any of the 5 other ways that real estate investors make money! Here are the calculations:

The numbers start to get silly when we have a moderate to aggressive outlook, that real estate value could rise, say an average appreciation rate of 5%:

When the value of the property went up 25%, the profit on the original $100,000 investment doubled.

There are two additional ways that inflation helps real estate investors.

Rent is a large component of the Consumer Price Index, CPI, which is the most widely used measure of overall inflation 4. So almost by definition, rents go up when inflation goes up.

This means that the rent you are receiving today will almost assuredly have the same real purchasing power in the future. And if rents go up faster than CPI, your future dollars will have even greater purchasing power than today.

Compare this to a fixed-income security, like a bond. When we buy bonds we know exactly what our future returns will be. But if inflation goes up faster than say the +/-1% that safe bonds are paying today, we are actually losing money.

And the third way inflation helps real estate investors is similar in concept, and relates to the time-value of money.

When we borrow money at a fixed rate, the money we use to pay it back in the future is less valuable than today’s dollars.

To continue with the earlier example, borrowing $300,000 today, at a 2% CPI inflation rate, is the equivalent of borrowing $271,719 five years from now.

Let’s use an example to illustrate this point: your rich and very generous friend offers to loan you $300,000 at a 0% interest rate, and she wants to be paid back in 5 years. You invest that money in starting a business, and in Year 5 hand her a check (with a a big hug and “thank you”) for $300,000.

But now when she goes to spend that $300,000, she can buy roughly the same equivalent that $271,719 buys today. Her dollars (or in our case the bank’s) are worth less in the future.

5. Tax Benefits of Real Estate

There are three major tax benefits to real estate investing. I will write in more detail about each of these in the future. This is a brief overview of:

Depreciation – straight line, accelerated, and bonus accelerated

1031 Exchanges

Opportunity Zone Investments

(NOTE: Several of my colleagues warned me about giving “tax advice.” All of these concepts are general, well understood tax advantages of real estate. Of course you need your own CPA, and of course this is general information, not tax advice specific to your circumstances. Disclaimer over.)

Depreciation:

Depreciation is an enormous benefit that isn’t widely understood. But you don’t need to be a CPA to understand, and once one does understand it, you’ll wonder why you haven’t been investing more money into real estate vs. other asset classes.Depreciation is a non-cash expense that our accountants include in our Profit and Loss Statements and tax returns. It is an enormous benefit because we pay taxes on our Net Income, and our Net Income is reduced and often even eliminated, by Depreciation. 5

This is precisely why many professional real estate investors pay very little in Federal Income taxes. Let’s go back to the $400,000 property example. Let’s assume this savvy investor has found a property at a 6.5% Cap Rate (see this article for a deep dive on cap rates and how to find 6.5% returns). The Net Operating Income is by definition $26,000 (Cap Rate = NOI / Value). After paying the annual mortgage, the investor put $6,674 in their bank account for the year. 6

Using straight-line depreciation, the most simple form of deprecation, the investor pays no tax on the income generated from the building. Hers is a simple P&L Statement to illustrate:

Pick your tax bracket – say 35%. By paying zero taxes on your $6,674, your essentially received a 35% higher return than a similar investment that is subject to your Federal Taxes.

Accelerated and Bonus Accelerated Depreciation will be discussed in a future article. Same concepts, but bigger tax advantages in the first year(s) of ownership.

1031 Exchanges

When real estate assets are sold, the IRS Tax Code 1031 allows investors to re-invest the proceeds into another “like kind” investment, and pay no taxes on the gain.

If an investor buys say Apple stock totaling $400,000, and sells it later for a $40,000 profit, the investor will pay a Capital Gain tax on the profit, even if it is re-invested in another stock.

The real estate investor who takes their proceeds and re-invests in another property (wisely using leverage to amplify their purchasing power), will not pay any Capital Gains tax. This allows them to keep growing their real estate portfolio, tax free!

Opportunity Zone Investments

Opportunity Zones are new to the tax law, and are meant to encourage investment and development in lower income neighborhoods.

Every state has designated census tracts (neighborhoods) that are located within an Opportunity Zone.

For people who invest and develop in these neighborhoods, an Opportunity Zone tax benefit is somewhat similar to 1031 exchanges. They allow the deferral of capital gains taxes.

The biggest difference – and new to the tax law – is that non-real estate assets can be sold, and invested into real estate. So back to our Apple investor, if she were to take her $40,000 gain and invest it in a property in an Opportunity Zone, and if they follow all the guidelines, they would delay and reduce their capital gains tax for many years.

There is much more nuance, complication, and rules around Opportunity Zone investments, far too much to cover in this article. You’ll need to work with your CPA on these, and there are plenty of published articles on Opportunity Zone investments that are worth researching. I’ve currently bought two Opportunity Zone investments, and am working with clients and investors to acquire more.

Conclusions:

Real estate is unique among investment asset classes, in that there are five different ways that investors make money.

Compare this to investing in stocks: a stock that pays a dividend and appreciates in value, generates two ways to make money. If that stock is bought within an IRA, 401(k) or other tax-advantaged account, there are three ways that stock investors make money.

But real estate is better than a 401(k), primarily for control and tax-free income that can be spent today, or re-invested for the future.

While other asset classes are eroded by inflation, real estate benefits from inflation. Real estate investments protect the investor’s dollars, so that future buying power is greater than it is today, not less.

And finally, think about this: what is your greatest expense? Hint: *taxes*

Through wise real estate investing, investors can reduce, and possibly even eliminate many of the taxes that otherwise erode our investment returns. This allows for much greater compounded returns over time.

When all 5 of these benefits are combined within one asset class – real estate – it’s no wonder that many of the world’s billionaires made a significant percentage of their fortune by investing in real estate.

A Primer on What’s Coming Ahead in the Commercial Real Estate Market

Part 2 in a Series: Investment Strategies for a Post-Peak Economy

Earlier this year, I published an article on where the for-sale residential market is heading, and strategies and outlooks for home buyers and home sellers.I updated that article after the Union Tribune published mid-year housing data by zip code.

Since publishing the original article, many of the predictions have played out: we are now mid-summer 2019, the prime buying season for residential real estate, and in San Diego and other markets, there continues to be flat pricing, an increase in inventory, and slower sales.

This article, Part 2 in a series, is focused on commercial property investing. Commercial properties are properties that generate income for the owner, unlike a home. Commercial real estate in this context includes: apartments, office, retail, and industrial.

We are going to take a hard look at the numbers in order to understand cap rates and mortgage interest rates, and how these two variables largely determine the price an investor is willing to pay for an apartment building or other type of commercial building.

The bottom line: in today’s market, property investors must be seeking CASH FLOW, above all other investment metrics.

The other major investment metrics, aside from cash flow, include: price appreciation (equity growth), tax benefits, loan paydown (equity growth), and a hedge against inflation. 1All of these are important. But in 2019 – 2020, Cash Flow is King.

Why is that? It is all about Cap Rates and Interest Rates. We’ll get into that. But first a quick discussion: I mean, isn’t it always about cash flow?

Not necessarily: there are markets, like San Diego and most of Southern California, the Bay Area, and New York, just to name a few, where there is rarely any immediate cash flow in commercial real estate investments. These are low cap rate markets.

People investing in those markets are rewarded by the other metrics, especially from rent growth and price appreciation. But now is a very dangerous time to rely on anything other than cash flow.

To understand why, let’s review what a cap rate is, and most importantly, what it means.

In plain English, the cap rate is the return, or yield, an investor will receive, if they buy a commercial building all cash, with no loan. 2

So if I pay, say $2MM for an apartment that generates $100,000 in Net Operating Income (NOI), 3 the Cap Rate for that building is $100,000 / $2,000,000 = 5%

So the equation of a cap rate can be written two ways:

Cap Rate = NOI / Value or…

Value = NOI / Cap Rate

These are the same equation, just re-arranged. If you know any two of the variables, you can solve for the third.

And here is a VERY IMPORTANT note: Cap Rates are determined by the market. So if I am an investor looking to purchase an apartment building, in a market where most apartments sell for, say 4% cap rates, then I can expect to pay a 4% cap rate, regardless of whether it’s a $750,000 acquisition, or a $3,000,000 acquisition. 4

And another important note: In the Cap Rate equation, the NET OPERATING INCOME (NOI) is assumed to be the actual performance of the building over the trailing twelve months. In other words, this number is a known entity, which determines the value of the building, depending on the current cap rate that investors are paying in the market.

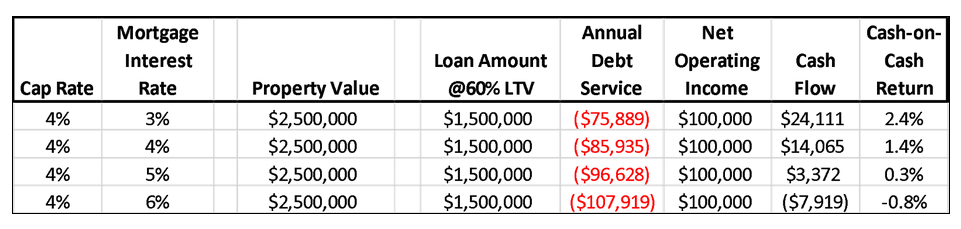

So here is how the value of an apartment building with a trailing twelve month NOI of $100,000 will change, depending on the cap rates that investors are willing to pay:

In San Diego, cap rates have been hovering around 4%. So an investor can expect to pay $2.5MM for a building that generates $100,000 in NOI.

And here’s where things get interesting: if-and-when cap rates rise by one percentage point, say to 5%, the value of that same exact building drops by a whole 20% — from $2.5MM down to $2MM!

So now let’s circle back to interest rates, and mortgage rates, in particular. We know that when interest rates, determined by the Fed, rise or fall, mortgage rates are correlated and also rise and fall. The two are not the same thing, but they tend to move together.

Interest rates are currently at a historically low level. This was part of the Fed’s response to the Great Recession. Low interest rates can encourage businesses and individuals to borrow money and invest, which leads to more economic activity – new buildings, new equipment that increases productivity and income, more home buying, loans and credit used for home improvements, and other job-and-income creating investments. These new jobs and income then have a multiplier effect on the economy, with more people spending more money.

In contrast, the Fed will typically raise interest rates when inflation starts to go above their target of 2% per year. Higher rates mean: less borrowing, less investment, and lower values in real estate.

As of this writing, the Fed just dropped their interest rate, and it is possible will drop again in 2019 and 2020. This is a reversal of the policy they started in 2018, to slowly increase interest rates.

As real estate investors, we are extremely sensitive to increases in interest rates, and we are invested for the long-term. 5 So even though rates may stay low through 2019, perhaps even 2020, we must be prepared for when (not if) they will increase. Historically low rates will eventually increase.

What Happens to Commercial Real Estate When Interest Rates Rise

As discussed above, when Cap Rates increase, the value of a commercial property declines. That’s just pure math. And it brings us full circle, back to the theme of this article: Why Cash Flow is King.

Going back to our example of a building that generates $100,000 in Net Operating Income:

If you bought it when cap rates are 4%, and you have a mortgage at say 3% (that’s super low, for example purposes, realistically it’s probably 4% or higher!), your cash flow looks like this:

In the example above, with a 3% interest rate, the property is only generating a 2.4% cash-on-cash return. The cash-on-cash is the cash flow after debt service, $24,111, divided by the down payment of $1,000,000.

So if you are an investor in San Diego today, you will find similar opportunities in a 4% cap rate market: a property that generates $100,000 in NOI will cost you $2.5MM, with at least $1MM down payment, and you will receive $24,111 after paying all property expenses plus your mortgage.

Now let’s look at what happens to the Cash Flow and Cash-on-Cash Returns when the mortgage rates increase from 3% to 6%:

Recall the Net Operating Income is the cash flow before debt service. It assumes the owner has no mortgage, since some buyers are all-cash, some buyers can get lower interest rates than others, and others might choose a low Loan To Value (LTV) mortgage, say 50% or 60%, instead of a high LTV mortgage. The cap rate values the property independent of the loan. But if you get a loan, of course you need to pay the mortgage from the cash flow of the property.

The Cash Flow plummets! Using the 5% interest rate row above, the property that cost $2.5MM is only generating $3,372 in annual cash flow to the owner. One roof repair, or water leak, and that property is losing money for the year. 6

But it gets worse.

As we discussed, when mortgage interest rates rise, usually cap rates rise. So right when the cash flow decreases or even goes negative for the year, the value of the building plummets, as well:

Revisiting the Cap Rate equation, the property that an investor paid $2.5MM for, and is still generating the same $100,000 in annual NOI, is now worth $2MM when market cap rates go up to 5%, and only $1.67MM when cap rates increase to 6%.

So now that investor may be losing money with negative cash flow, and the value of the building has dropped. If they need to sell the building, they will lose the equity that they invested in the $1MM down payment. The sales price of $1.67MM pays off the loan of $1.5MM and pays for the transaction costs, commissions, and legal work needed. But almost the entire $1MM original investment is lost.

Even worse, this scenario can lead to foreclosures and bankruptcy.

Here’s Why Cash Flow is King

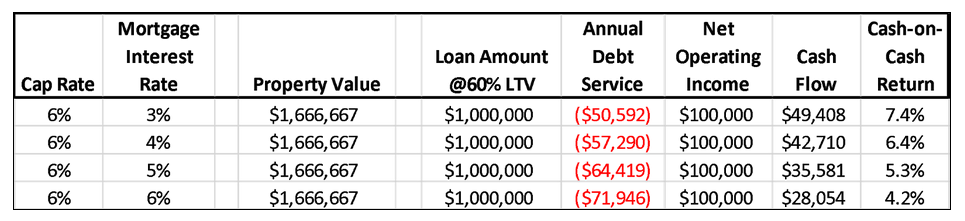

Now let’s look at an investor who purchases a property outside of a low-cap rate market like San Diego, New York, San Francisco, Los Angeles, and other markets.

Believe it or not, there are cities where investment properties trade at cap rates of 6%, 7%, and even 8% or higher. These cities are likely smaller, non-coastal, and have fewer real estate investors competing to purchase commercial properties. But they exist!

And….higher cap rates can also be achieved by investing in mismanaged, value-add properties with low rents. (more on that below)

So let’s compare the downside protection that a building with strong cash flow provides:

In a market where 6% cap rates are normal, a property generating $100,000 in NOI will cost $1.67MM to acquire.

And the Cash Flow, even when mortgage rates rise to 6%, is great:

Most importantly, if cap rates rise above 6%, and therefore the value of the property drops below $1.67MM, the investor is protected because, as long as they’ve locked in a mortgage rate as high as 6% (way above current rates), they can still service the loan, make plenty of cash flow every year, and there is no need to sell the property for a loss.

So How Do Investors Find 6% or Greater Cap Rate Properties?

All this math is great, in theory, but in a 4% cap rate environment, it may seem like wishful thinking. Experienced investors may be thinking: Great, but where can I find a 6% cap rate property?

There are two primary ways to find cap rates 6% or greater. The first is:

Find properties that are being mismanaged, have high operating expenses, and/or rents that are below market.

These properties are usually off-market, meaning not listed with a big brokerage, and the owner is self-managing the property instead of working with a professional property management team.

These will typically require a substantial additional investment to bring the properties up to contemporary finishes, add new amenities, or make other improvements in order to raise the rents and decrease operating expenses, resulting in a scenario like these:

The property acquired at a 4% cap rate is now generating a 5% or even 6% yield – as the owner’s new cap rate, after the buyer raised rents and decreased costs by investing an additional $200,000 into the property.

And here’s how much value those improvements created. Assume that the overall market is still selling at 4% cap rates. With the new Net Operating Income of either $135,000 or $163,000 as shown in the example, the property is now worth:

Therefore, the value created (profit) under these two scenarios is: 7

So by finding a mismanaged, value-add property, injecting $200,000 to improve it, and raising rents and decreasing expenses, the value has gone way up and the cash flow is now much higher. That investor can sell for a big profit, or hold the property long term for cash flow. Their downside is protected!

Should I buy Class A or Class C? Often the properties that trade at the lowest cap rates are considered “Class A.” This means they are the newest, in the best locations, with the best interior finishes and property amenities. There is very little “value add” opportunities to Class A properties. Investors who purchase these properties do so because they view them as “safe” and are willing to take a lower return for the perceived lower risk. But the exact opposite is true!

Without a value-add component, the Class A property, purchased at a 4% cap rate, with top-of-the-market rents and efficient operations through professional management, will be hit the hardest in terms of both cash flow and value, when interest rates rise.

The second way investors can find cap rates of 6% or greater is to go outside of San Diego and other low-cap rate markets. In many cities, 6% or greater is the norm!

I will talk about these markets in future articles. But one tip: I have personally invested in a Mid West city that has great economic indicators, has a growing population and jobs, and 6% or greater cap rates are the norm. In fact, if one looks hard enough, even 8%, 9%, and 10%+ cap rates are achievable in this market.

Conclusions

This article is meant to give all real estate investors – beginning, intermediate and experienced – the mathematical explanations on why Cash Flow is King in the current economic cycle.

There are many metrics that investors use when evaluating an investment property. These include: cash flow, price appreciation, tax benefits, and inflation hedges. I will discuss these in greater depth in my next article in this series.

In a low cap rate and low mortgage rate environment, investors can see their cash flow eroded and the values plummet if interest rates tick up by just 1% or 2%.

Properties with strong cash flow, generally defined as cap rates at least 2% higher than the current mortgage rates, are insulated from the macro-economic risks of rising interest rates. These properties:

Can continue to service their debt and make the owner a positive annual cash flow

If values go down because interest rates go up, there is less risk of foreclosure. The owner does not need to sell, and can continue to hold the asset for the long term

The opposite occurs when investors acquire properties in a low cap rate, low mortgage rate environment, as we’re currently experiencing. Investors face great downside risks:

No cash flow, and not being able to pay the mortgage

Plummeting property values when interest rates tick up 1% or 2%

Risk of foreclosure and even bankruptcy

Investors can find better cap rates, even in a low cap rate and low interest rate environment, by:

Buying value-add properties, and increasing the Net Operating Income

Investing in non-coastal markets, where cap rates are generally higher

About MV Properties and Keegan McNamara:

MV Properties exists to serve our clients in building their wealth through real estate investments.

We guide our clients through creating customized real estate investment strategies.

We analyze our clients’ portfolios, looking at Return on Equity, debt strategies, and tax efficient planning, to develop a plan specific to each clients’ needs.

We let the numbers tell us the strategy, as each situation is different.

Keegan McNamara is a real estate investor, developer, and broker. He owns MV Properties, a residential brokerage and property management firm, and McNamara Ventures, a development and investment company. Keegan can be reached at keegan@mcnamaraventures.com

[ 1 ] My next article in this series goes into greater depth on these concepts, it is titled “5 Ways Real Estate Investors Make Money.”

[ 2 ] We build in financing assumptions after the cap rate calculation

[ 3 ] Net Operating Income is defined as the total income from the property in a given year, minus all of the costs to operate that building, except debt service. These costs include: property taxes, property management fees, repair expenses, utility costs, landscaping, marketing, and other property-level expenses.

[ 4 ] That’s a mild over-simplification: apartments in more desirable locations, and newer buildings, will sell for lower cap rates, all else being equal, to apartments in worse areas or older buildings that may be due for major maintenance.

[ 5 ] Real estate assets are illiquid, and often have big pre-payment penalties on the mortgages. So as investors, we must plan to own the asset for several years at a minimum. Contrast this to say, a publicly traded stock, which can be bought or sold 24 hours a day, 365 days a year.

[ 6 ] Experienced real estate investors know that Debt Coverage Ratio (DCR) is an important factor in determining the loan amount, LTV. The above example assumes the original loan was made at 3% floating rate, at a DCR of 1.32x, and the rate subsequently rose to 5% or 6%.

[ 7 ] “Profit Upon Sale” is simplified and does not include transaction sales costs, nor the positive cash flow that was generated to the owner.

With historically low unemployment and interest rates, we would expect to see prices rising. And in some neighborhoods, they are (see the great charts in the UT article). In others, prices are down slightly.

So for folks looking to sell their home, move-up, move-down, or get out of the market completely, what is a good strategy?

The conclusions from my article in May still hold:

San Diego is a supply-constrained market, which will always put upward pressure on prices

Short term blips are not likely to re-create the tremendous buying opportunities we saw in 2008 – 2012

Your home is an illiquid asset that you live in – it’s not a stock to trade

So if your family circumstance dictate that now is a good time to buy / sell your home, that should be the #1 deciding factor

Waiting to time the market is not a winning strategy.

MV Properties is here to guide our clients through these decisions. We think about real estate obsessively, and create strategies specific to each of our clients’ needs.

If you are thinking about buying or selling a home, let’s talk and developyour strategy for building wealth through real estate. MV Properties’ boutique realtors will execute that strategy for you.

About the Author

Keegan McNamara has over 20 years’ experience in all aspects of real estate development, investment, consulting, and management. Mr. McNamara is the owner of www.mcnamaraventures.com and www.mvproperties.com.

Mr. McNamara is a licensed real estate broker and holds an MBA in Finance from UC San Diego’s Rady School of Management, and undergraduate degrees in Economics and English from Occidental College.

Earlier this year I had the honor to host a client appreciation night for MV Properties’ investors, partners, clients, and friends. At the event, I presented “Investment Strategies for a Post-Peak Economy.”

I’d now like to share some of the highlights of that talk, and discuss how we are guiding our clients in executing these strategies – so that they will build long-term wealth for their families.

The Cycle

Before diving into Investment Strategies for a Post-Peak Economy, it’s important to understand the premise of the title of that speech, and what the numbers are telling us about this business cycle.

One of my first lessons in this business is that real estate is cyclical, and that as investors we should do our best to understand where we are in that cycle, and plan accordingly.

So where are we today? Is it time to buy, hold, or sell real estate?

The first question is easier to answer, so let’s start there. In this article I’ll discuss the housing market, and then in upcoming articles, the investment property market.

In San Diego, it is now officially a buyer’s market. The numbers are in, and for people selling their home it is taking longer, there is more inventory competing for buyers, and we are seeing price adjustments downwards. As-of this writing, the County-wide pricing is down at least 7% from the peak last summer.

Each neighborhood and market segment will vary slightly from that number, some with greater price cuts, and some with less.

We are still up, very slightly, year-over-year. But just barely. Meaning home prices a year ago were 1%-2% higher than today, which sounds reassuring, but the trend is moving downwards: a year ago prices continued to climb, peaking in the summer of 2018, and then started moving downwards.

So is this the beginning of a correction, or a blip on the radar prior to the summer selling season?

My answer: it shouldn’t really matter. Your home is a huge investment, but it is much more than that. Timing the market perfectly is less important than finding the right home for you, at the right time in your life. If I felt another 2007-2011 style price drop was coming, that would change the recommendation. But I don’t.

At our Client Appreciation Night, I showed the following chart:

If you had held off buying a home in 1991 because you felt we were at a peak, and wanted to wait for the really great deals to come along, you were right! But you had to wait for 7 years, as prices bumped along a bottom before turning back up.

And in the meantime, you would have missed 7 years of living in your home. It’s a home, not a share of Apple stock. A home isn’t just a pure investment! Using economists’ terms, we “consume” our home. That’s a weird way to say that we are building memories, raising a family, and getting to know our neighbors.

But from a purely financial perspective, the buyer who didn’t wait, and who purchased in 1991, built equity through paying the mortgage. So a buyer’s timing in 1990 wasn’t great, but over the next 7 years they built more equity up than the amount they saved by waiting to buy at the absolute bottom. They were better off financially not trying to time the market.

And – for those looking to time the market, remember: we are still at 3.7% unemployment in San Diego. Job growth is what fuels the demand for housing. As a region, have more available job positions than qualified people to fill them.

So while we are seeing an increase in the supply side, leading to softening prices – and that may continue – the demand side is as strong as it’s ever been.

It is a safe time to buy. And if your life circumstances dictate that it is time to sell, there are still plenty of buyers. You just need to adjust your expectations – it’s no longer a frenzied market, with multiple offers the first day.

MV Properties is here to guide our clients through these decisions. We think about real estate obsessively, and create strategies specific to each of our clients’ needs.

If you are thinking about buying or selling a home, let’s talk and developyour strategy for building wealth through real estate.

MV Properties’ boutique brokerage has the two best agents in San Diego, Todd and Rena Bell. They truly appreciate the opportunity to serve you on your journey to wealth building. www.bellteamhomes.com

I personally work with select clients on multi-family property sales and acquisitions. I’ll write more about that market in an upcoming article. I’m also a developer and investor myself, and will discuss the strategies my partners and I are executing.

Reach out to me, or Todd and Rena, today so that we can guide you through a long term strategy of building wealth through real estate.

Next Article, Part 2 in a Series: The Investment Real Estate Cycle

Many landlords and rental property owners wonder whether it’s better to hire a property manager or take care of the property on their own. Today, we are explaining why you it’s better for you and your investment to hire a professional property manager.

If you’re an investor and a property owner and you already have rental properties, you know how much work it can be. A professional manager can save you time and resources by finding the right tenants, screening those tenants, making sure everything possible is being done with advertising to ensure the listing is getting out to the widest possible pool of potential tenants and keeping track of market rents in your area and for your particular property type. That is a lot of work in itself.

If there is a unit that turns over, you need carpet cleaners, painters, and other contractors to make the place ready for the market again. Property managers work with the best professionals in the business and you can benefit from the savings that come from our relationships with those vendors.

When a unit turns over, we systematically line up all the repairs and start marketing the unit immediately. We are often able to minimize a vacancy period to a matter of days, whereas most DIY owners/landlords take at least a month to fill a vacancy. Think about that: 1.5 months vacant / 12 months per year equates to lost revenue of 12.5% – that’s less than our management fees! Just by minimizing vacancy periods, our services more than pay for themselves.

The best part of having a property manager working on your behalf is that you get your time back. You don’t want to be called in the middle of the night or over the weekend for an emergency repair. If a hot water heater starts leaking or the air conditioning breaks down, your property manager will get that call and take care of the problem on your behalf. All you have to do is collect a rent check that we wire to you once a month. A good property manager will also provide a full financial statement, including invoices and receipts for every penny that’s been spent. Companies like ours are transparent and efficient. Your CPA will appreciate our reports!

Hiring a professional property manager will earn you extra income on your property. In the first year of operation, even after paying our management fee, our clients have seen their investment income go up an average of between 10 and 30 percent.

We always recommend that you use a professional company to manage your rental home. If you have any questions or you’d like to hear more about the services we provide, please contact us at MV Properties.

It’s that time again – one of your renters is vacating their unit and you have to make the tough decision of picking a monthly rent for your property. This is a decision not to be taken lightly – if you pick a rent that is too low for the market, you could be leaving thousands of dollars on the table over the life of the lease. But if you aim too high, your unit could sit vacant longer, costing you money every day that it is empty. At MV Properties, we can walk you through the basics of hitting that sweet spot for market rent to maximize the value of your rental property.

Scope Out the Competition

In order to best understand the rental value of your property, you need to get familiar with the other properties your potential tenants may be checking out. Think like a renter; understanding the market comparables is the key to knowing how to price your unit.

Explore other available housing options in the building and nearby, checking popular rental websites such as Craigslist, Trulia, and Apartments.com. Make sure that when you are evaluating a comparable property, you make adjustments for special features that may be different than your property, such as better views or valuable amenities like off-street parking or a gym. Consider which special features may lure a renter to your property – especially your property has something that may be worth charging a little extra.

Call in the Experts

San Diego is a large area full of unique neighborhoods where the rental market can vary greatly from across a few miles. For example, the average rent in 2015 for San Diego County was $1,856 per unit, but if you narrow it down by neighborhood, rents ranged from an average of a whopping $3,334 in Del Mar Heights to a more reasonable $1,180 in Barrio Logan. An important key to pricing your rental property correctly is to tap into the knowledge and experience of a professional property manager.

At MV Properties, we know that understanding the demographics, history, and competing projects in a neighborhood can be crucial to pricing a rental property effectively. A neighborhood like the Downtown market is historically a luxury market that demands high rents, but a glut of new development in 2016 can constrain rents when new rental competition hits the market.

These factors can affect pockets of the neighborhood differently, sometimes changing from one building to the next. Having a knowledgeable, local representative will keep you aware of the fast-moving market and trends that can affect your property’s value.

Pricing Philosophy

Once you have a ballpark figure based on comparable units and an understanding of the market, you should consider your pricing philosophy. San Diego County is one of the tightest rental markets in the Country, with historical vacancy hovering around just three percent.

Because of limited options, rents have been rising steadily in the area, with rents increasing an average of 5.3% between 2014 and 2015 alone. As an owner, that gives you options to follow trends and raise your rents accordingly, or you can raise rents more slowly in order to attract and retain more stable, long term tenancy. Sometimes, demanding higher rents can beget more demanding tenants!

Let Us Help

Now that you understand the factors that affect market rents, call MV Properties at 888-686-1525 to help you reach your property management goals. From providing up-to-date and in-depth market knowledge to ensuring a smooth and stress-free transition between tenants, we can help maximize your rental investment. Ask a question anytime by emailing keegan@mv-props.com and visit our website to learn more.

About Keegan

Keegan McNamara is the founder of MV Properties, a leading San Diego property management company offering the highest level of service in property management, maintenance, and leasing. His goal is to cultivate long-lasting relationships with his clients (property owners) and their tenants to provide an enjoyable leasing experience. Keegan holds a Masters in Business Administration from the Rady School of Management at UC San Diego and is a Principal at McNamara Ventures, a real estate development, and investment company focused on residential and mixed-use properties.

Insurance is incredibly important to anyone with assets to protect, especially rental property owners. The wonderful world of insurance is complicated, convoluted, and can be difficult to navigate for those unfamiliar with coverage and gaps. As a rental property owner, it’s important to make sure you hold the right coverage, and that your renters and property managers hold adequate coverage as well.

Insurance for Property Owners

Although most homeowners have a homeowner’s insurance policy, many rental owners may not know if their standard policy covers when their property is rented. Many homeowner’s policies may cover short-term rentals up to a few weeks, but could be voided if the property is not primarily owner-occupied.

The homeowner’s insurance company may deny coverage if your policy does not cover a rental. Policies for rental units have various names depending on the company, but they generally are referred to as dwelling policies, and fall into three categories: DP-1, DP-2 and DP-3.

A DP-1 policy is basic and covers simple things like fire and vandalism. DP-2 policies are broader, and cover named perils like damage from a windstorm, hail, fire or vandalism. Some even have a provision for a collision, such as if a car were to hit the property.

Finally, a DP-3 policy is a ‘special form’ or an ‘open peril’ policy. Unless a peril is specifically excluded, it’s covered. The different policies will also cover the property to different degrees. With a cheaper DP-1 policy, the property may only be covered for existing value, whereas a more broad DP-3 policy would cover replacement value.

Existing value means that you would only be paid what the property is worth, not the full cost to replace it. For example, if the roof were 10 years old, existing value would not pay out the cost to install a new roof, the payout would be written down for the 10 years of age for the damaged roof.

Obviously, a DP-3 policy will be the most comprehensive and provide the best coverage in the case of an emergency, but is likely the most expensive coverage as well. The savings on the less expensive policy could be offset in a tragic event, where the less expensive policy does not cover your lost rental income during a rebuilding period. It’s important for property owners to balance the investment of insurance with a policy that will protect them from catastrophic loss.

What About Your Renters?

Although a comprehensive landlord insurance policy will cover your property in the event of damage, most renters are completely unaware your policy does not cover any of their belongings. If your unit were to burn in a fire, the standard landlord policy would only cover the cost of the structure, not any of the items inside.

For this reason, many landlords require their tenants to maintain a renters insurance policy throughout the term of their lease. Unlike the property policy, renters insurance is generally very affordable, often less than $20 a month depending on the value of the renter’s items. An added bonus of a renter’s insurance policy is that they typically cover the renter’s items regardless of location. So, if their laptop was stolen from the library instead of the rental unit, the policy would typically still cover it. Property owners would have to maintain a separate personal property insurance to get the same amount of coverage.

Even more important for property owners, if a rental unit is damaged due to negligence of the tenant, the landlord can often place a claim on the tenants’ insurance, rather than their own. For example, if the tenant leaves a stovetop on and burns the kitchen, the claim on their renters policy will save the owner from potentially higher insurance premiums in the future.

What About Property Management Insurance?

After obtaining quality property owner coverage on a unit, most landlords may think they are done with their insurance needs, however, this can be a costly mistake. Professional property management companies often carry insurance that can be extremely valuable in protecting their property owners from lawsuits or damages.

The policies usually include a general liability policy, as well as a professional liability policy called errors & omissions or “E&O”. Property managers, like doctors, lawyers, and architects, need E&O insurance because the decisions they make can cause damages and cost lives if they are negligent.

Even if a property manager properly fixes any outstanding hazards, E&O is still important to defend management and the landlord from litigious tenants, bystanders, or visitors to the unit. The general liability coverage they carry is also extremely important; covering landlords if they’re sued for damages including an indoor fall, an animal bite, or someone slipping on a wet sidewalk.

Working with a professional property management company not only minimizes the danger of liability claims by proactively maintaining your unit, but also by ensuring that you, your tenant, and property management company are fully covered from any dangers that may arise. If you are looking for a fully insured and professional property management company in San Diego, contact MV Properties today!

Let Us Help

If you are concerned about the liability or insurance needs of your rental, call MV Properties at 888-686-1525. From providing up-to-date and in-depth regulatory knowledge to ensuring a smooth and stress-free transition between tenants, we can help maximize your rental investment. Ask a question anytime by emailing keegan@mv-props.com and visit our website to learn more.

About Keegan

Keegan McNamara is the founder of MV Properties, a leading San Diego property management company offering the highest level of service in property management, maintenance, and leasing. His goal is to cultivate long-lasting relationships with his clients (property owners) and their tenants to provide an enjoyable leasing experience. Keegan holds a Masters in Business Administration from the Rady School of Management at UC San Diego and is a Principal at McNamara Ventures, a real estate development, and investment company focused on residential and mixed-use properties.

Simply put, a Capitalization Rate, or Cap Rate for short, is the return on an investment when you divide the Net Operating Income (NOI) by the price you are paying for the property. For example, if you purchased a property for $2 million dollars and produced an NOI of $100,000 annually, it would be considered a 5 percent cap rate.

Net operating income (NOI) is simply the annual income generated by an income-producing property after taking into account income collected from operations and deducting all expenses incurred from operations. These expenses include property taxes, utilities, repairs, maintenance, and property management fees. They do not include debt service, since some owners may pay all cash, while others take advantage of low interest rates and maximize the loan on the property.

What Does a Cap Rate Mean?

Cap rates are often used to compare similar properties that could not be valued using the traditional “Comps” of residential real estate. For example, if I’m looking to buy a home in a specific neighborhood and I’m considering two houses, I can quickly understand the value of the home by seeing what similar sized homes in that neighborhood have recently sold for, and adjusting for things like pools, the age of the home, etc.

However, when evaluating an investment asset, it can be substantially harder to find similar properties and assign a quantitative number to their differences. And since what one is really buying is a future stream of rental cash flows, not a residence to live in, it is necessary to underwrite the expected Yield on the investment. Cap Rates are one measure of investment yield.

A cap rate, as a measure of return, is far more valuable to an investor who may be analyzing two different apartment complexes on different sides of town. By researching the properties’ NOI and dividing by their purchase prices, it is easier to choose which may prove to be the better investment.

Generally speaking, the more desirable and less risky a property, the lower the cap rate and therefore the higher the price relative to the NOI. Today, an apartment near the beach may sell for a 4% cap rate, while properties in secondary markets where the perceived risk is higher will sell for higher cap rates and therefore lower prices.

Cap Rate as a Means to Add Value

One thing we specialize in at MV Properties is identifying ways to add value for our clients and their real estate assets. Most people do not think of cap rates in this manner, but here is an example:

We recently added a laundry room to a property that did not have any laundry facilities. The total cost of the addition and the coin operated washer and dryer was $15,000.

We were then able to raise rent on all five units by $200 per month – the desirability of the property went up and so the tenants were willing to pay a lot more. Who wants to spend their weekend at a laundromat?

We also collect approximately $200 per month in laundry income.

The total addition to the property’s Net Operating Income is $1,200 per month or $14,400 per year. The addition pays for itself in just about one year!

But even more importantly, that $15,000 addition just added $288,000 in value to the property!

Assuming a 5% cap rate of $14,400 / 5% = $288,000.

That’s a 19.2X multiple on the invested capital!

This is not a subjective valuation like a sales comp – it is the quantitative method appraisers and buyers use to value rental properties.

How Does My Property Compare?

At MV Properties, we are experts at Maximizing our clients’ cash flow, and preserving and enhancing the long-term value of their real estate assets. The large multiplier effect of cap rates means that it is imperative you maximize your Net Operating Income! To get a free benchmark report to see how your property measures up, contact us today!